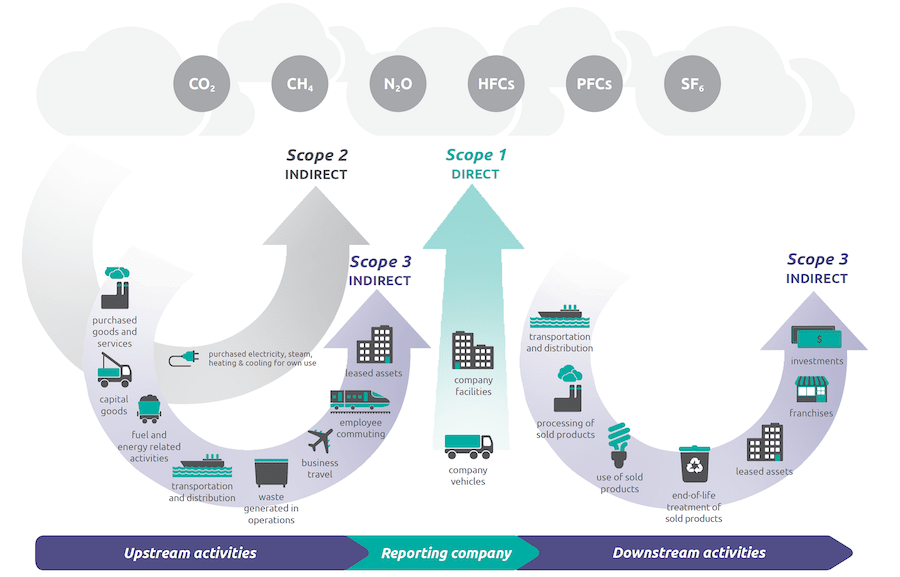

Scopes 1, 2, and 3 of Carbon Emissions

Decreasing carbon emissions is quickly becoming not just a matter of corporate social responsibility for businesses but a necessity. Companies need to take stock and understand their carbon footprint to reduce emissions or reach a carbon-neutral status. Doing so requires understanding the scope 1, 2, and 3 type emissions involved in their central operation and upstream and downstream value chains.

As was abundantly clear during the COVID-19 pandemic, any disruption to global markets and supply chains has far-reaching effects on a company’s ability to operate and its bottom line. Climate change resulting from the emission of greenhouse gases will lead to more uncertainty in markets through increased extreme weather events and the displacement of hundreds of millions of people globally. Those companies that follow the GHG protocol will be better adapted to future changes and help prevent the worst-case scenarios.

In this article, you will learn:

- What the GHG protocol is

- What scopes 1, 2 and 3 mean

- The importance of the GHG protocol

What is the GHG Protocol?

The Greenhouse Gas Protocols are the most widely accepted international accounting tools for governments and corporations to “understand, quantify, and manage” their emissions. These protocols were established by the World Resources Institute and World Business Council for Sustainable Development in 2001. Most national emission accounting tools are based on this international protocol, allowing for a global standard in assessing an industry’s environmental impact and carbon footprint.

The GHG protocols apply to the direct and indirect emissions of carbon dioxide, methane, and other GHG gasses produced through the full cycle of a business’s activities. Various processes and sources are divided into 3 scopes, simply named Scope 1, Scope 2, and Scope 3 of carbon emissions.

What are the 3 Scopes of the GHG Protocol?

Accounting for the greenhouse gas emissions of any industry or company is highly complex and involves both direct or indirect sources and upstream and downstream sources.

For this reason, the sources are broken down into three scopes, with Scope 1 being the easiest to understand and quantify and Scopes 2 and 3 being slightly more complex.

Scope 1: Direct emissions

Direct sources of emissions are accounted for in scope 1 and pertain mostly to sources owned or operated by the business. Direct sources of emissions include three main categories:

- Fuel Consumption

- Company Vehicles

- Fugitive Emissions

Direct fuel consumption involves all the fuel used for processing or to power a company or industry, such as the furnaces used to melt metal in the steel industry or the boilers used in chemical processing plants. These sources are apparent and easy to quantify.

Company vehicles include the vans and trucks used to transport and distribute the products and goods that the business creates. Again, this is readily measurable as there will be a line item on the expenses for fuel purchases for these vehicles.

The last direct emission, fugitive emissions, includes leaks of greenhouse gases, such as the hydrofluorocarbon (HFC) refrigerants in freezers and air conditioners. While these gases are generally less abundant than carbon dioxide or methane, they are hundreds to thousands of times more potent than CO2 in trapping heat in the atmosphere. Each year, the supermarkets in the US leak enough HFCs to equal the GHG emissions of 12.5 million passenger vehicles.

While scope 1 emissions are the most readily observable and measurable for many businesses, they are not the largest sources of emissions in their industries. For commercial buildings in the US, scope 1 emissions accounted for only 20.4% of the total. In most corporate settings, the indirect emissions amount to a much larger environmental impact than the direct ones that usually get the most attention.

Scope 2: Indirect emissions

The indirect emissions included in scope 2 relate to all the emissions from energy used to power everything the company owns. This includes all the electricity, heat, steam, and cooling purchased by the company to run its operations. These emissions are generally accounted for through on-site use or upstream of manufacturing.

Like scope 1 emissions, this is fairly easy to visualize, measure, and quantify as most companies understand how much energy they purchase. It is also being addressed through the rise of renewables or offset by capture and storage schemes.

For many manufacturing industries, scope 2 has the highest carbon footprint. Likewise, it is the highest for commercial buildings in the US, accounting for 48% of the total GHG emissions produced.

Together, scopes 1 and 2 comprise most of the energy use and other factors contributing to greenhouse gas emissions and a company’s localized carbon footprint. What has not yet been considered are all of the externalities of the input resources and outgoing services and products.

Scope 3: Upstream and downstream emissions

Scope 3 of the GHG protocol opens the accounting process much wider and internalizes many of the indirect processes that do not necessarily occur on-site. These include both upstream and downstream sources.

Upstream sources include much of the energy, transportation, and manufacturing that goes into the business or industry to support its function. Some examples of this include:

- Business trips and stays

- Employee commuting

- Production of fuels and products the company uses

- Capital goods (buildings, vehicles, and machinery used by the company)

- Leased assets

- Chemical reagents

- Packaging

- Transportation of purchased goods and resources

Also included in Scope 3 are the indirect downstream processes that result from the goods or services produced by the reporting company. Examples of these include:

- Packaging and transportation of goods

- Processing and use of sold products

- Franchises energy use

- Product disposal

- Investments

Scope 3 is extensive and seeks to make companies accountable for producing, using, and disposal of their products. Scope 3 is an important part of assessing a company’s environmental impact by evaluating every stage of a product’s life cycle.

The Importance of the GHG Protocol

To accurately assess the carbon footprint of a company or industry, it must take into account all three scopes. The largest environmental impacts would be missed by focusing only on the direct and localized sources of GHG emissions.

It is too easy for companies to hide their indirect impacts, like beverage companies promoting their recycled plastic utilization but not reporting that 91% of their bottles are never recycled after use.

To truly understand, account for, and address carbon emissions, each company needs to assess all three scopes in their entirety as their primary sources can vary widely.

For example, a building’s scope 3 emissions are about twice as high as their scope 1, while the transportation industry can attribute about 70% of emissions as direct, i.e., scope 1. While the construction industry has very few direct emissions, the indirect supply chain (scope 3) emissions are immense.

Identifying and accounting for all three scopes of greenhouse gas emissions has transformed how carbon footprints are assessed. This system will continue to be refined and improved upon to help companies understand and reduce the environmental impact to limit the worst-case scenarios of climate change.

If you enjoyed reading this article, you can read more related content here: